BoC vs. Fed: What Today’s Rate Decisions Mean for Investors

On January 29, the Bank of Canada (BoC) and the Federal Reserve (Fed) made their latest interest rate decisions, highlighting a growing divergence in monetary policy between the two central banks. The BoC reduced its overnight rate by 25 basis points to 3%, marking its first rate cut in this cycle, while also announcing the end of quantitative tightening. This decision reflects a combination of factors, including inflation nearing the 2% target and concerns about the potential impact of trade tariffs on the Canadian economy. Meanwhile, the Fed opted to hold its benchmark rate steady, remaining cautious as U.S. inflation has proven more persistent. Policymakers are also assessing the economic implications of policy shifts under the new administration before making any adjustments. This difference in approach highlights the evolving economic conditions in both countries and sets the stage for potential policy shifts in the coming months.

BoC and FED policy rate - Source: Trading Economics

Inflationary trends and labour market conditions have played a key role in shaping these policy decisions. In Canada, CPI inflation eased to 1.8% in December 2024, remaining close to the BoC’s target range. Meanwhile, the labour market has softened, with 6.7% unemployment and wage growth moderating. The BoC’s latest Monetary Policy Report projects GDP growth of 1.8% in both 2025 and 2026, though these projections do not account for the potential imposition of U.S. tariffs. In contrast, U.S. inflation remains stickier, with CPI inflation holding at 2.9%, above the Fed’s 2% target. The U.S. labour market remains resilient, with unemployment steady at 4.1%. The Fed remains attentive to economic momentum, particularly as it assesses the impact of fiscal policy under the new administration.

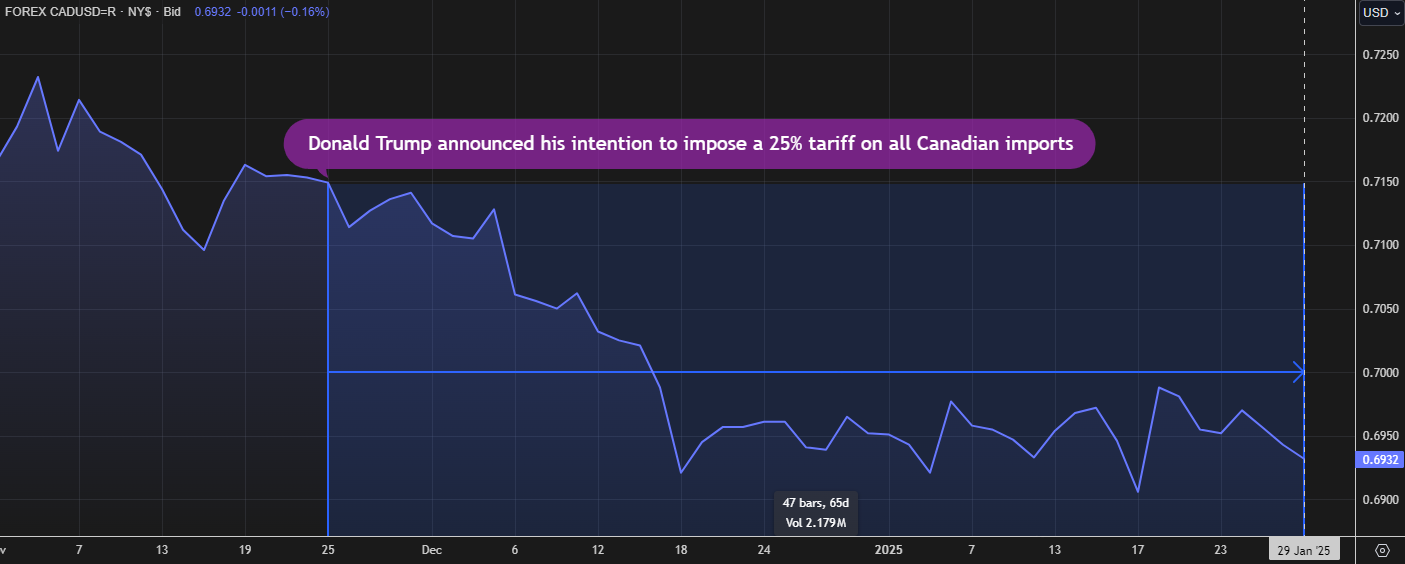

One of the key risks to both economies is the potential for new U.S. trade tariffs, which could heavily impact Canada, as around 75% of its exports go to the U.S. The BoC has acknowledged that its forecasts do not account for these tariffs, which could disrupt supply chains and dampen growth. Should tariffs be imposed, Canada’s economy will be tested for resilience, as weaker external demand could weigh on exports and business investment. For the U.S., while tariffs aim to protect domestic industries, they could increase costs for businesses reliant on imports and lead to supply chain inefficiencies. The U.S. dollar has strengthened in recent weeks as investors view its economy as more insulated from external risks. The Canadian dollar, in contrast, has weakened slightly against the U.S. dollar, reflecting concerns over reduced export demand, higher costs for businesses, and weaker investor confidence from trade policy changes.

CAD to USD FX - Source: LSEG

Looking ahead, economic uncertainty remains high in both Canada and the U.S. The BoC expects inflation to remain near its target, but the trajectory will depend on external risks such as trade policy and global demand. The central bank has signalled that it remains open to further rate cuts should economic conditions warrant them. Meanwhile, the Fed is proceeding cautiously, emphasizing data dependence and the need to see further progress on inflation before making any policy changes.

Market expectations for future rate moves reflect these differences in central bank positioning. There is a 42.2% chance of another BoC rate cut in March, especially if trade tensions intensify. For the U.S., markets assign a 26.9% probability of a Fed rate cut in March. Instead, market pricing indicates that U.S. rate cuts are more likely to begin in June, with a 47.3% probability assigned to a move at that meeting. Upcoming data on inflation and trade will be key in shaping future rate decisions for both central banks.

World Interest Rate Probability - Source: Bloomberg - January 29th, 2025

World Interest Rate Probability - Source: Bloomberg - January 29th, 2025

If you have any questions about today’s Market Update, feel free to call us at 604-643-0101 or email cashgroup@cgf.com .

Market Updates

Our market commentary breaks down the latest business, financial and money news. If you’d like to receive all of our market update emails, send us an email by clicking the subscribe button. If you found this content helpful, share it widely!