The Rising Cost of Borrowing for British Columbia: A Closer Look at Debt, Credit Ratings, and Market Trends

British Columbia, like other provinces, funds a portion of its operations by issuing bonds - debt instruments purchased by investors in exchange for regular interest payments. While this process rarely makes headlines, the cost of borrowing is a critical financial consideration for any government. It directly impacts how much the province pays to access capital and, ultimately, how much taxpayer money is spent on servicing debt. In recent years, BC’s borrowing costs have quietly increased, driven by a combination of shifting credit ratings, market dynamics, and comparative disadvantages relative to larger provinces like Ontario.

In 2017 and into mid-2018, BC was able to issue 10-year debt at significantly lower rates than Ontario, despite being a smaller issuer. On June 6, 2018, the spread between BC and Ontario’s 10-year bonds reached a low of -13.09 basis points, meaning BC was paying over 13 basis points less than Ontario to borrow. This reflected BC’s AAA credit rating at the time and strong market confidence in its fiscal position. Since then, that advantage has gradually eroded. As of April 2025, BC now pays approximately 2.5 basis points more than Ontario to issue comparable debt - a total swing of just over 15.5 basis points from the 2018 low. A timeline of the BC–Ontario 10-year bond spread from April 2017 to today clearly shows this reversal, with the turning point emerging shortly after mid-2018.

Source: Bloomberg BRCOL 2.55 06/18/27-ONT 2.6 06/02/27

This shift in spread translates into tangible costs for the province. According to BC’s Budget and Fiscal Plan, over the next two years, BC is expected to issue or renew approximately $50.70 billion in debt. This includes, among other obligations, $8.23 billion maturing in March 2026 and $6.35 billion in March 2027, alongside a $14.30 billion in new borrowing to cover this year’s deficit (estimated by Moody’s) and an additional $10.20 billion projected for the following year. If all of this debt is issued on 10-year terms at today’s spread - 15.5 basis points higher than the most favourable point in 2018—it would result in an estimated $78.59 million in additional interest annually compared to what BC would have paid had it been borrowing at that 2018 low. That translates to roughly $1.51 million per week in extra taxpayer costs over the next decade.

Understanding why this spread has widened requires looking at one of the key drivers of borrowing costs: credit ratings. The highest rating, AAA, indicates minimal credit risk and allows issuers to access funding at the lowest possible rates. BC held this top-tier rating for many years - longer than any other province following the global financial crisis - while others, including Ontario and Quebec, were downgraded. This advantage helped keep BC’s borrowing costs exceptionally low. Over time, however, that position began to deteriorate as the province’s fiscal outlook weakened and deficits grew. In April 2025, both Moody’s and S&P Global downgraded British Columbia’s credit rating on the same day, Moody’s from Aaa to Aa1, and S&P from AA- to A+, citing a growing debt burden and persistent structural deficits. Moody’s, for its part, projected a $14.3 billion shortfall for the current fiscal year, well above the $10.9 billion forecast provided by the provincial government.

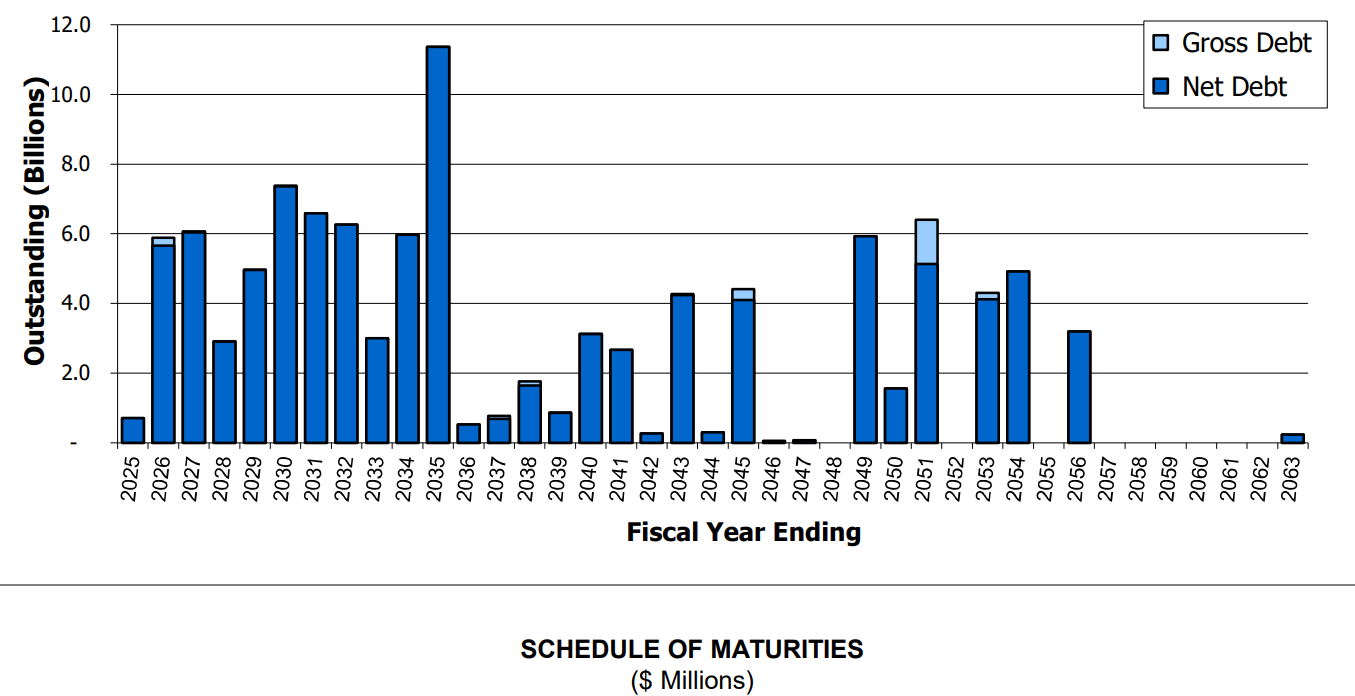

As of September 30, 2024, BC’s total debt stands at approximately $116.5 billion. Unless the province returns to surplus and begins paying down principal, that figure will continue to grow. Most of the debt is long-term and will come due gradually over the next 30 years. The chart below illustrates the province’s debt maturity schedule, highlighting a steady stream of refinancing needs in the years ahead. Meanwhile, regaining a top-tier credit rating is not something that can happen overnight - it requires years of consistent fiscal discipline and strong economic performance.

Source: Net debt maturities Schedule - Government of British Columbia

Market Updates

Our market commentary breaks down the latest business, financial and money news. If you’d like to receive all of our market update emails, send us an email by clicking the subscribe button. If you found this content helpful, share it widely!